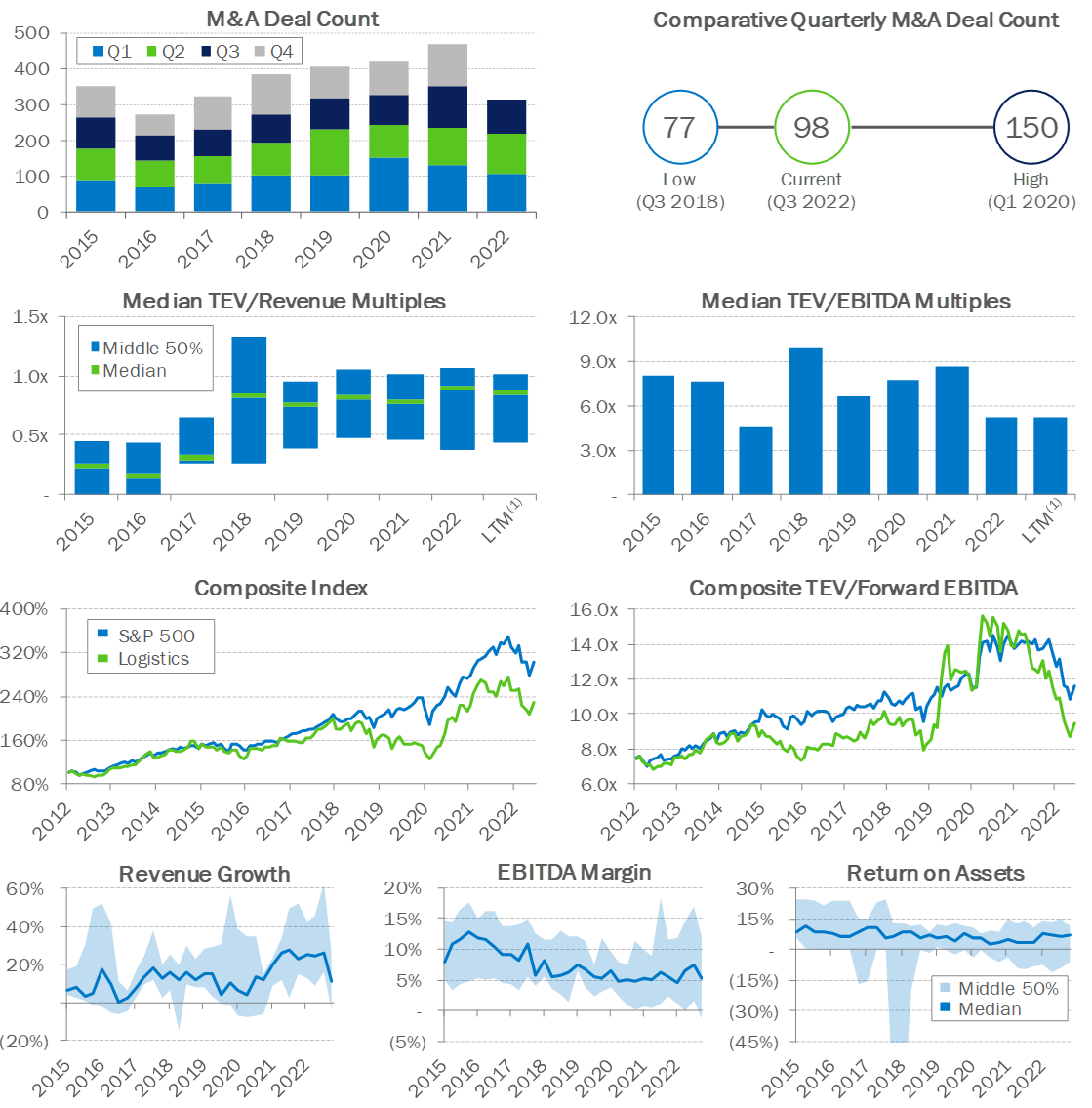

With 98 reported transactions globally in Q3, activity in the sector remains firm. However, YTD deals fall 97 below the respective 2021 count.

Pricing for services in sub-sectors most impacted by the recent supply-chain disruption and port congestion are moderating, despite the continued shutdowns in China. This has reduced revenue growth and compressed EBITDA margins.

Logistics and Transportation, a pillar of the world economy, remains a fragmented sector. Operators continue to seek economies of scale, while new entrants and specialized players continue to develop innovative and tailored service offerings. These trends create an environment prime for consolidation, where we continue to see activity from a healthy mix of strategic and financial buyers.

As consolidations play out and competition to acquire attractive companies is intense, we also see caution with buyers wanting to avoid overpaying. These concerns are mainly motivated by rising interest rates, recession fears, and geopolitical uncertainty.

.png)